Why Fund Accounting Makes Restricted Funds Easier to Manage

If you’ve ever tried to keep track of restricted donations using a mix of color-coded spreadsheets and a little bit of hope, you know how quickly things can get complicated. Restricted funds play a big role in carrying out your organization’s mission, but they can also create stress for finance professionals, especially for those who are newer to nonprofit accounting or coming from a for‑profit world where “funds” work differently.

Managing funder‑restricted dollars becomes much easier with the right accounting structure and software. When your system is designed to track restrictions clearly, it’s simpler to stay compliant, maintain accurate balances, and give colleagues the insight they need into how restricted assets are being used.

This guide breaks down what restricted funds are, why they’re tricky, and how fund accounting software simplifies the entire process. Whether your role is strategic or hands‑on, you’ll walk away with practical examples you can apply right away.

Why Restricted Funds Are Challenging to Manage

Restricted funds are donations or grants that must be used for a specific purpose and exactly as directed by the donor or funder. They are a promise: “We’ll use this money only for the reason you intended.”

For example, if a donor gives $50,000 to support your summer meals program, you can’t use those dollars to repair your roof or upgrade office tech. You must track them separately, report on them accurately, and release them only when used for the intended purpose.

For new nonprofit finance professionals—especially those with a for‑profit background—this is the moment these accounting processes start to feel different. Instead of one retained earnings bucket, you suddenly have to track multiple net asset categories, each with its own rules.

Restricted funds introduce several day‑to‑day complexities:

1. You’re tracking Multiple balances at once.

You need to maintain the organization’s overall net asset balance, and a separate, accurate balance for every restricted purpose.

Traditional accounting systems aren’t built for this. They expect all activity to roll up into one balance. That’s why so many organizations end up managing restrictions in spreadsheets outside their system.

2. Every restricted expense requires an extra step.

If you are managing restricted funds, a typical process in a commercial accounting system might go like this:

- Record the expense

- Figure out manually whether restricted funds apply

- If they do, create a release from restrictions

- Update the spreadsheet that tracks remaining balances

Multiply that by every grant, program, and restricted gift, and it’s easy to see how the workload grows for your financial team managing these restricted funds, and how errors creep in.

3. Spreadsheets can’t maintain internal controls.

When different people update different tabs, it’s hard to ensure your formulas are consistent and your balances are up to date. When you don’t know who changed what and when, it’s difficult to create clean audit trails.

This is exactly why many organizations struggle. Not because they lack skill, but because the tools they’re using weren’t designed for restricted fund management.

Why Fund Accounting Software Solves These Problems

Fund accounting is a system where you track financial activity based on both how funds are used and what they are used for. It’s widely used in nonprofits, educational institutions, and government agencies because it organizes financial activity into discrete buckets—funds—that maintain their own balanced ledgers.

Fund accounting’s power becomes even clearer when you add two key capabilities:

1. Subfund OR Program Records

Instead of creating a brand‑new fund structure every time you receive a restricted gift, subfunds allow you to track the purpose of each restriction, the balance available, and the activity flowing in and out.

All without expanding your chart of accounts.

2. A Segmented Chart of Accounts

Segments let you code all these in one flexible string:

- Fund

- Natural Account Code

- Program

- Grant

- Department

Your accounting team stays organized across a more organized chart of accounts by leveraging consistent building blocks, and reporting becomes far more meaningful.

Together, these capabilities eliminate the need for spreadsheets, extra releases, or guesswork. Every transaction contains the information it needs to land in the right place—even complex ones.

How Fund Accounting Works in Practice

With a fund accounting system, each subfund or program has its own self‑balancing record. Restrictions are embedded into the accounting structure, and you no longer have to manually track where restricted money lives.

Communicate Restricted Balances by Program

Many parts of your organization rely on restricted fund management, including your program team and leadership.

Imagine a program director who wants to send a member of their team to a conference to learn about a new delivery model. If their program has unused restricted balances available for that specific purpose, the trip might be feasible. If not, the cost pulls from unrestricted funds, which may be needed elsewhere.

A fund accounting system lets you easily drill into balances by subfund or program, so you can quickly see which activities have remaining restricted support. You can also identify which expenses have already been applied to that fund, and share reporting with program managers without spreadsheet gymnastics. It’s like each of your programs has its own set of balancing books to report from whenever you need.

This helps teams make faster decisions backed by reliable data.

Ensure Accurate Data for Better Decision Making

When you manage restricted funds in a system designed for them, you don’t have to create workarounds just to create a report. Your chart of accounts is manageable, you have transparency into how funds were spent, and you can quickly pull accurate reports for funders and your stakeholders.

Here are a few ways a fund accounting system helps you improve the accuracy of your financial data.

1. Stop creating new funds for every purpose

You don’t want to create a separate fund for each possible activity your organization engages in, but you still want to be able to break down that restricted balance by its purpose. What’s a CFO to do? Use subfunds.

A fund accounting solution with subfund capabilities can not only take the guesswork out of how to manage it all, but it can also ensure you’re always making decisions based on current, accurate balance information, without having to reconcile with external spreadsheets first.

2. Get instant visibility into restricted balances

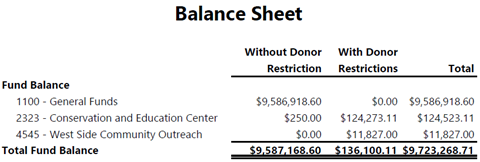

Fund accounting software that allows your programs to retain equity gives you an instant snapshot into which subfund or program “own” what portion of the fund balance. Then, in one report, you can get an instant restricted net asset balance on the level of detail that is meaningful to you.

3. Code activity at the level of detail you need

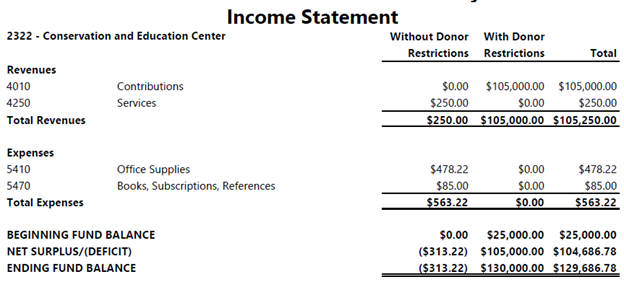

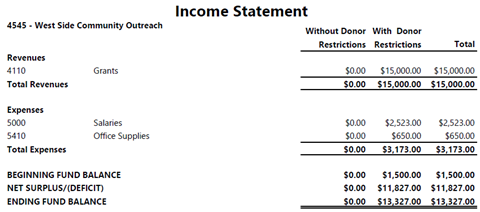

Traditionally, you’d need to juggle spreadsheets or comb through a general ledger report to figure out whether each expense transaction would be covered by restricted funds. But with the subfund record capability of fund accounting software, you can code your activity with the level of detail needed to identify what areas of your mission it relates to, allowing you to run reports reviewing both summary activity and detail.

This income statement displays activity in one program area. Based on the “With Donor Restrictions” fund balance, you can see the full amount of expenses can be covered by funds restricted to this purpose.

Release Restrictions Without the Busywork

Instead of managing releases one transaction at a time, fund accounting software lets you adopt more efficient workflows.

Option 1: Bulk Releases

As expenses come in, code them using unrestricted expense accounts and the appropriate subfund record. At month‑end, or any interval that works for you, run reports to calculate total activity as well as restricted and unrestricted net asset balances, such as the income statement above. Then create one journal entry batch to release it. Attach the supporting income statements or GL reports for audit‑ready documentation.

Option 2: Direct Coding to Restricted Funds

If most or all your expenses will be covered by restricted dollars, or if you’ll be verifying availability of restricted funds before entry, you can record the expense directly to the restricted fund. The system maintains the balance automatically, ensuring everything stays in balance.

While this option is not standard for fund accounting, with self-balancing software tracking net asset classification within funds, you can let your software maintain the balance for you. This is especially helpful when you know most of your transactions are covered by restricted funds, because it eliminates the need to monitor and reclass the restricted balance. Your finance team is empowered to efficiently track your spending and report on net asset balances in real time.

How Fund Accounting Helps with Internal Controls and Audits

Managing your restricted funds directly in your accounting software allows you to apply system-based internal controls and simplify your audit prep, saving you time and minimizing risk. Here are a couple of examples:

1. Reduce manual reconciliations

Every spreadsheet you eliminate is one less potential source of error. Tracking your restricted funds directly in your accounting system streamlines your data entry and makes reconciliation easier and faster.

2. Strengthen role‑based controls

Because restrictions are built into the accounting structure, coding becomes more consistent. Role-based permissions mean only approved team members can make changes to what expenses are placed in what fund—and not whoever can access the spreadsheet.

3. Improve audit trails

Subfund activity provides clear visibility into which funds were used, when releases occurred and for what expenses, and how balances changed. Attached documentation makes it easy for auditors to confirm those transactions.

4. Simplify reporting

Fund accounting systems produce clean, defensible statements that align naturally with nonprofit reporting standards—including FASB ASC 958. When you are juggling multiple spreadsheets to track your grants and other restricted funding, it can take hours just to get a budget to actual comparison.

Fund Accounting Systems Support the Way Your Organization Actually Works

Managing restricted funds becomes far less stressful when your accounting system is built to support the way mission-driven organizations actually work. A purpose‑built fund accounting solution gives you confidence that every dollar—restricted or unrestricted—is tracked accurately and consistently, without the manual workarounds that create risk or slow your team down.

When your processes for managing restricted funds live inside your fund accounting software rather than scattered across spreadsheets and shared drives, the entire operation becomes more streamlined. Releases are easier to manage, reporting is more intuitive, and your team can focus on supporting the mission rather than stitching together data. A strong fund accounting foundation creates a level of clarity and accountability that builds trust across your organization and with the people who support it.

If you’re ready to move away from spreadsheets and into a system built specifically for nonprofits, join us for an on-demand product tour of Blackbaud’s fund accounting solution, Blackbaud Financial Edge NXT®.

Common Questions About Restricted Funds

What is a restricted fund?

A restricted fund contains donations or grants that must be used for a specific purpose defined by the funder. Often, the fund broadly indicates whether restrictions apply to the dollars, with subfunds representing programs or activities owning portions of the balance to indicate what specifically the money is restricted for.

How do you track restricted funds?

The easiest way is to use a fund accounting system with subfund capabilities and a segmented COA to maintain balanced ledgers for each restricted purpose. Otherwise, you will likely need to rely on spreadsheets or an inflated chart of accounts to track your restricted funds.

How do you release restricted funds?

Either bulk‑release restricted activity periodically or code expenses directly to the restricted fund if supported by your system.

Why Shouldn’t I track restrictions in spreadsheets?

Many nonprofit organizations, government entities, or educational institutions do track their restricted funds in spreadsheets, especially if they are using a commercial accounting system. But spreadsheets create audit risks, inconsistent controls, and manual workloads that grow unsustainably as your organization scales.

What reports help with restricted funds?

Income statements by program, GL detail reports, and fund balance summaries showing restrictions by purpose.