GAAP for Nonprofits: Why the Numbers Differ and How to Explain the Gap to Your Board

Have you ever had your board members scratch their collective heads when the development and finance teams report their results? Do you get questions on why the two never match up?

The quandary that faces every nonprofit management team is how to communicate the difference in GAAP to non-GAAP operating results. In many respects, it is the same challenge our for-profit friends face when they eliminate stock-based compensation from their financial statements, except in nonprofit accounting our challenges are on the revenue side of the equation.

With good training, clear reporting, and a little patience, you can help your nonprofit Board members understand the difference between the GAAP results your accounting team needs and the non-GAAP results presented by other areas of the organization.

GAAP for Nonprofits: What It Gets Right and Where Boards Get Lost

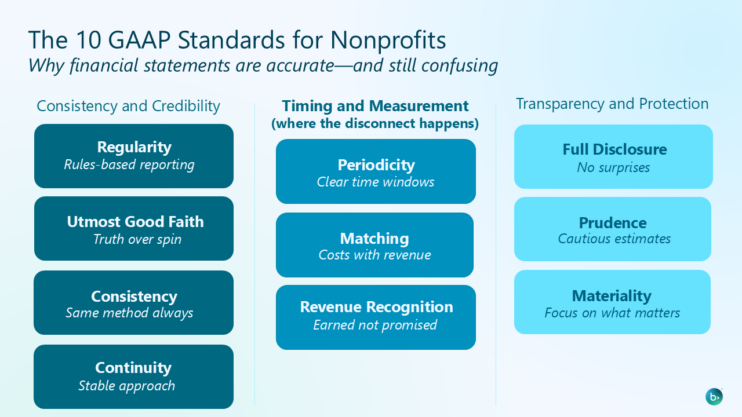

GAAP—generally accepted accounting principles—gives nonprofits a consistent, credible way to report financial performance. It’s ten standards create a shared language for auditors, regulators, and finance leaders, and it helps ensure that financial statements reflect what’s earned in a given period, not just what’s received. In short, GAAP is designed to protect transparency and trust.

Where boards often get lost is that GAAP is doing exactly what it’s supposed to do—just not what they expect it to do.

Under GAAP, nonprofits use accrual accounting. Revenue is recognized when it’s earned and measurable, not when it’s pledged, promised, or anticipated. That’s why certain types of revenue that feel very real to development teams don’t show up the same way in GAAP financials. Bequests, insurance policies, and some planned gifts may represent significant future value, but they aren’t reflected in GAAP results until the organization has a legal right to the funds.

This is often where the questions start.

A development report might highlight a major win—say, an insurance policy naming your organization as a beneficiary. From a fundraising perspective, that’s worth celebrating. From a GAAP perspective, however, the timing matters. If the donor is 45 and very much alive, the organization hasn’t earned or received that revenue yet, so it doesn’t belong in GAAP results. Both teams are right, but they’re answering different questions.

GAAP also requires nonprofits to track restricted funds separately to honor donor intent. Dollars raised for a specific program or purpose can’t be treated as general operating revenue until those restrictions are met. Again, this is a strength of GAAP. It enforces discipline and accountability. But to a board member scanning high-level numbers, it can look like money is “missing” or unavailable without clear explanation.

So when boards compare development totals to GAAP financial statements, the mismatch can feel confusing or even concerning. The reports are correct, but your board need a translation. And without a clear way to reconcile the two views, finance leaders are left repeatedly explaining why the numbers don’t line up.

Educating Your Board on GAAP for Nonprofits

My first couple of board meetings as a CFO were spent going down the rabbit hole of explaining why my development partners reported these great multi-million-dollar quarters, and I would show the board just how little cash came into the door and how much of that could actually be spent on the operations of the organization.

So, what can you do to eliminate these uncomfortable conversations?

Educate, educate, educate. Do you have board members who are members of the business community or are they from other disciplines that never have the need to understand a financial statement? Depending on their comfort discussing financial statements, craft a workshop that helps them not only understand the differences in not-for-profit versus for-profit accounting, but also what is considered a gift by your development staff versus what hits your financial statements.

- Does development count expectancies and bequests at face value or a discounted rate—do they record them at all?

- Do your development partners count conditional pledges?

- How do you explain the discount rate on multi-year pledges?

These are all areas that impact the variance between what you’re reporting and what the development office reports out.

Create a Simple Reconciliation Schedule

This type of GAAP‑to‑non‑GAAP reconciliation doesn’t require you to completely overhaul your financial statements. It simply bridges how results are reported internally and externally.

The simplest solution I found (after educating my board on the above issues) was to create a simple schedule that reconciled the non-GAAP development numbers back to what was reported in the financial statements.

The top of the schedule listed all GAAP revenue, including pledges, cash gifts, non-cash gifts, and irrevocable trusts. The report would show the subtotal of this revenue, and list the non-GAAP gifts below, such as bequests and revocable trusts. The total of the schedule then matched the numbers reported by the development team. Use clear labeling so your board members can easily see what is GAAP and what is non-GAAP.

By creating a simple, easy to follow reconciliation schedule, my development partner and I were able to clearly communicate the organization’s financial progress to our board.

Adhere to GAAP Standards with Fund Accounting Software

When you are focused on transparency and stewardship, you need to be able to track your revenue by fund and create reports to clearly show your financial data. Nonprofit accounting software allows you to track and report on your different funds, grants, programs, and projects in real time. It also integrates with your fundraising tools and automates the reconciliation process. With nonprofit accounting software, you can save time, reduce errors, and communicate your financial results clearly and confidently to your board and stakeholders.

How Development and Finance Can Get Along (Really!)Does your organization need a fund accounting system that makes it easy to adhere to GAAP reporting standards? Check out our buyer’s guide to help you make an informed decision about your accounting software.