Don’t Fear the Fraudster: Three Ways to Prevent Fraud at Your Nonprofit

Occupational fraud is a chilling reality for businesses and organizations of all sizes and occurs across industries—even within the nonprofit sector.

According to the Association of Certified Fraud Examiner’s (ACFE) 2018 Report to the Nations, 9% of occupational fraud cases took place at charitable organizations, resulting in a median loss of $75,000—the lowest of the industries represented in the study. However, these losses can make a tremendous difference for many nonprofits.

“For some a [loss of] $75,000 may be insignificant, but for many nonprofits, financial resources are extremely limited and a loss of $75,000 can be particularly devastating.”—Jonathan T. Marks, CPA, CFF, CFE, A Violation of Trust: Fraud Risk in Nonprofit Organizations

How Does Fraud Happen?

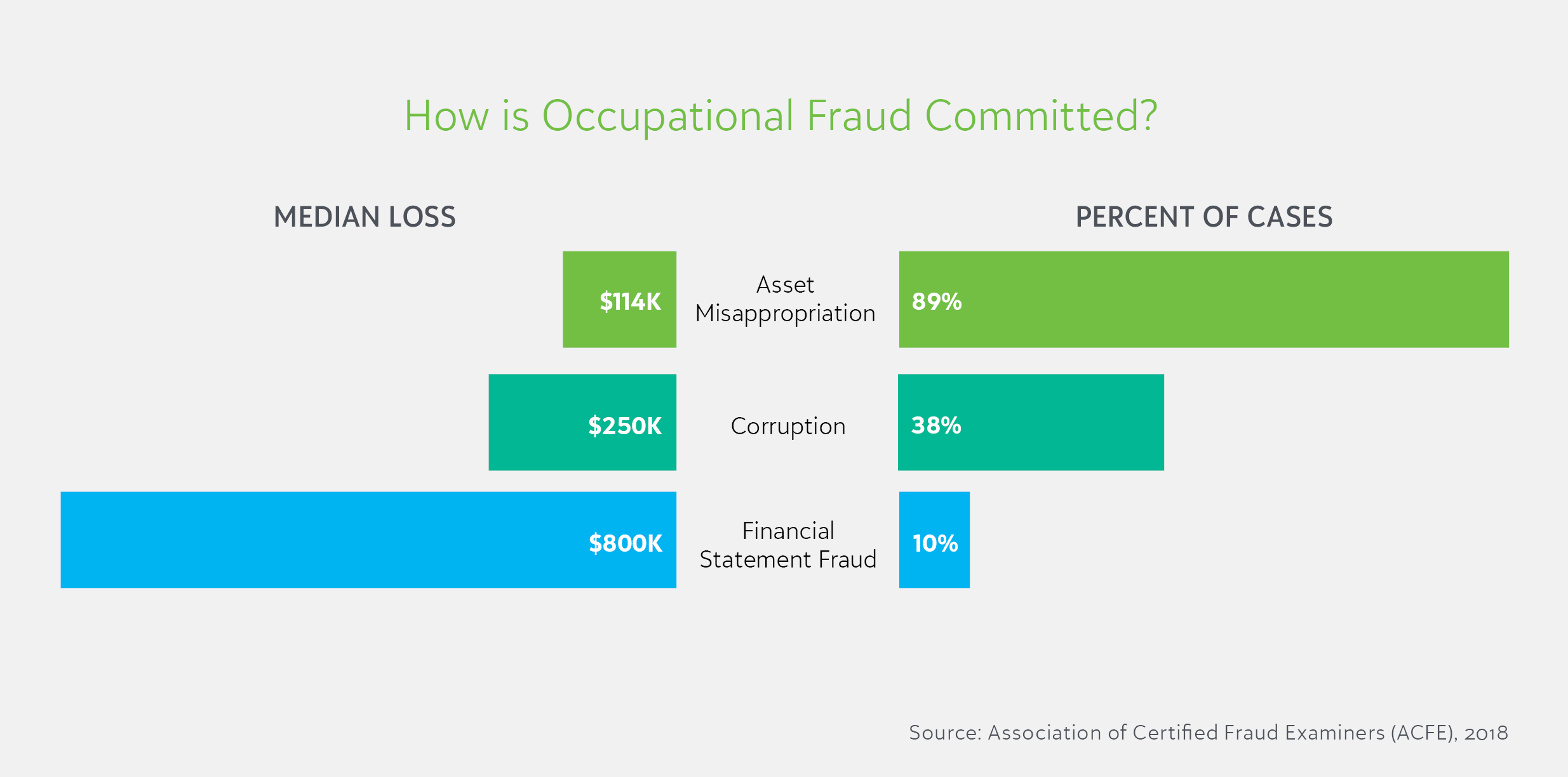

ACFE’s report cites the three most common types of occupational fraud as asset misappropriation, corruption and financial statement fraud. Financial statement fraud occurs least frequently of the three types, making up only 10% of cases, but results in the greatest median loss at $800,000.

While asset misappropriation leads to the lowest median loss at $114,000, it happens in 89% of cases making it the most commonly occurring form of occupational fraud by far.

The True Cost of Fraud

These statistics are alarming. However, the full impact of fraud is still unclear. The fact is that no one knows how many fraudsters manage to remain under the radar or even how many cases go unaddressed or unreported each year.

You may be wondering why, upon detecting fraud, any business or charitable organization would leave the situation unreported or unaddressed. And in many cases, it’s because of fear.

Because nonprofits are held to an especially high ethical standard, the potential consequences of fraud can be detrimental. Even one case of financial corruption or abuse can permanently tarnish the reputation of an organization resulting in loss of funding or even revocation of tax-exempt status.

Yet, the fears associated with fraud are the very reasons that nonprofits must take a proactive approach to detecting and preventing fraud.

According to an article published by Philanthropy News Digest, “Today’s public seems to be highly unforgiving of nonprofit institutions that breach their trust. In a climate of media-inflamed low public trust of charities, organizations must take action to prevent fraud and abuse before their reputations and financial support are irreparably damaged.”

How Can Fraud Be Prevented?

To nurture the trust that can be so quickly dissolved by the bad deeds of a few individuals, organizations must institute strong internal controls and fraud policies coupled with proper training for employees as well as technology systems that support these prevention efforts.

1. Internal Controls

According to Investopedia, “Internal controls are the mechanisms, rules, and procedures implemented by an [organization] to ensure the integrity of financial accounting information, promote accountability, and prevent fraud.” Examples of internal controls include:

- Separation of duties ensures that no individual is solely responsible for executing a financial transaction from start to finish. For example, the person who signs a check should not be the same person who writes the check. Having multiple signers is a plus!

- Regular and timely bank reconciliation provides an opportunity to review transactions and bank balances so any unusual activity can be spotted and investigated.

- Petty cash controls establish rules on things like the maximum amount of available petty cash as well as who has access to use those funds and who is responsible for approving disbursement. These controls should also document requirements and processes for approval requests (e.g., setting expense limits and requiring a receipt for every transaction).

Monitoring Financial Statements: as we previously mentioned, financial statement fraud has the potential to hit your finances the hardest, and it can be incredibly difficult to detect due to efforts by fraudsters to conceal suspicious activity. Instituting a process for reviewing financial statements and ensuring that the committee or individuals responsible for reviewing financial statements for anomalies have proper knowledge and training on what to look for will drastically improve the likelihood of detection.

2. Anti-Fraud Training

An important part of any fraud prevention program is training. All employees—including managers and executive leadership—should be mandated to participate in the training program to ensure that everyone in the organization is educated on all policies and procedures related to fraud prevention, detection, and reporting. Employees should be able to answer the following questions:

- What is fraud?

- How is it damaging for the organization?

- Who commits fraud? How do they commit fraud?

- What behavioral and financial indicators could point to potentially fraudulent activity?

- What are the organization’s fraud policies? What are the consequences for committing fraud?

- How can I report suspected fraud?

As reported by ACFE, 40% of fraud detection was the result of a tip—the most common method of detection. Empower employees by giving them proper training and a way to report suspected fraud safely and without the risk of retaliation.

3. Technology

To support your fraud prevention efforts, it’s critical to adopt financial technology that can help you monitor risks and enforce your control activities.

- Access Controls: Ensure segregation of duties in your financial system by controlling user rights. An advanced technology solution will allow administrators to configure user access at a granular level—from limiting who has rights to edit data to defining specific fields and transactions that can be edited (or even viewed) by individual users.

- Approval Rules: Your financial management software should allow you to configure a seamless approval path where you can require, review, and approve any documentation for expenditures requested by your employees.

- Bank Account and Credit Card Integration: Being able to view real-time bank and credit card information directly within your organization’s financial system can be hugely beneficial to catching suspicious activity early. Live bank and credit card feeds can allow approved financial staff to securely review the most up-to-date activity from your financial institution and compare that information to what has been recorded in the system.

The True Value of Fraud Prevention

“No social arrangement can operate well or for long without trust.”—Jeff Polet

While there are many obvious benefits we could touch on here, ultimately, it’s the ability of social good organizations to foster relationships built on trust—internally as well as with supporters, funders, and the people they serve—and continue the good work they do in the community that is at the heart of fraud prevention.

Proper controls, training, and supporting technology will help your organization create a culture of transparency and trust. Ongoing monitoring and upkeep of your fraud prevention program will keep your organization on track to maintaining its reputation as a good steward so it can continue to create positive change in the world.

Want to learn more about how to prevent fraud at your organization? Join Melissa and Julia at bbcon in Nashville for their session “Fraud Prevention: How Blackbaud Financial Edge NXT® and Best Practices Can Help You Prevent Fraud.” Register today!