Ensuring Utilization of Spendable Funds in Endowment Management: A Practical Guide for the Finance Office

Accurately identifying and utilizing your endowment’s spendable balances is one of the most powerful ways your organization can strengthen donor trust, maximize mission impact, and ensure long-term compliance.

Endowment managers are expected to demonstrate not only careful stewardship but also how these funds actively support the organization’s mission. When you and your stakeholders have a clear, shared understanding of what is available to spend, everything becomes easier. You can confidently honor donor intent, stay aligned with regulatory expectations, and proactively support the programs, people, and communities your organization serves.

Strong spendable balance management is a strategic advantage that fuels your mission and secures the long-term health of your endowment.

Understanding Spendable Funds

Spendable funds are the portion of an endowment that your organization can use based on donor intent, your organization’s spending policy, and applicable laws like UPMIFA. In other words, they represent the dollars your mission can put to work today. While that sounds straightforward, determining the true spendable amount is often more nuanced than people expect.

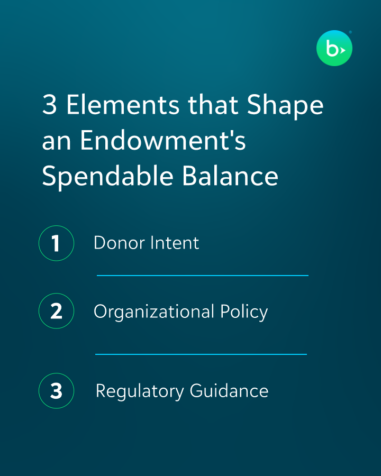

An endowment’s spendable balance is shaped by three key elements:

- Donor intent: What the gift agreement allows or restricts

- Organizational policy: How your institution defines and calculates spending balances

- Regulatory guidance: Particularly UPMIFA, which emphasizes prudent spending and protecting the fund over time

When these pieces come together smoothly, identifying spendable dollars is simple. But in reality, endowments often include decades-old gift agreements, earnings that fluctuate with market performance, and spending policies that evolve over time to keep pace with financial needs. This means the finance office is constantly navigating layers of history, policy, and compliance.

For example, a donor establishes a scholarship endowment where only the annual spending allocation—not the corpus—may be used. The organization has implemented a policy that only 4% of the average earnings over the past six quarters may be allocated to be spent. To calculate the spendable balance for this fund, you must:

- Track the original gift (corpus) to ensure it remains intact.

- Maintain accurate records of cumulative earnings, including both realized and unrealized gains.

- Calculate the six-quarter average market value, which smooths volatility across varying investment returns.

- Apply the 4% spending rate to that average value to determine the current year’s allowable spending.

- Assess whether the fund has experienced a temporary deficiency, which may limit or adjust spending in accordance with UPMIFA.

This process reflects donor intent, your internal policy, and prudent stewardship. But it also shows how dependent spendable balances are on accurate tracking, updated valuations, and clear communication.

Understanding spendable funds requires more than applying a percentage to an endowment balance. It requires the ability to clearly distinguish between the original corpus, cumulative earnings, and the portion that is truly available to spend. When finance offices maintain this level of clarity, the entire process becomes easier: calculations are more accurate, conversations with stakeholders are more straightforward, and compliance questions are far simpler to navigate.

The Impact of Inadequate Systems: Risks and Missed Opportunities

Managing spendable balances with outdated or fragmented systems creates operational and strategic problems that ripple far beyond the finance office. When you aren’t sure about how much of the fund is available for current projects, your organization could leave important funds idle. Money that could have powered scholarships, research, or community initiatives remains unused because no one maintains a clear, real-time picture of available resources.

When endowment data lives in spreadsheets, email threads, and disconnected reports, the organization loses the ability to see a reliable picture of what is actually available to support its mission.

Manual processes introduce several risks:

- Data inconsistency: Multiple versions of spreadsheets, copied formulas, and ad-hoc calculations make it difficult to confirm whether a number is current, correct, or based on the right source.

- Delayed information: If calculating spendable balances requires gathering files, reconciling discrepancies, or rebuilding reports, program leaders don’t get the information when they need it, and planning suffers.

- Limited transparency: Without clear, system-generated visibility into corpus, earnings, and spendable amounts, stakeholders cannot easily verify how much is available to make informed decisions.

- Higher audit exposure: Incomplete tracking or unclear documentation makes it harder to demonstrate compliance with donor intent, spending policies, and UPMIFA. Auditors naturally raise more questions when the supporting evidence isn’t centralized or consistent.

These challenges have real consequences. Scholarships may not be awarded because staff are unsure whether funds are available. Departments may hesitate to launch new initiatives because the financial picture is unclear. Donor-restricted funds can sit idle simply because no one has an accurate, timely view of what can be spent.

The impact on communication is just as significant. When the finance office struggles to explain the numbers in a timely manner, stakeholders lose confidence. Development teams struggle to steward donors effectively. Leadership receives an incomplete understanding of the institution’s capacity to invest in key priorities.

Ultimately, inadequate systems create inefficiencies, and they limit an organization’s ability to fully leverage its endowment. Without dependable, repeatable processes for calculating and communicating spendable balances, the organization risks leaving mission-critical dollars on the table.

How Fund Accounting Simplifies Utilization of Spendable Funds

Purpose-built fund accounting systems give finance teams the structure and visibility they need to manage endowments with accuracy and confidence. Instead of relying on spreadsheets or piecemeal tools, these systems organize endowment activity in a way that mirrors how the nonprofit actually operates: by fund, by purpose, and by donor intent.

Functionality in systems like Blackbaud Financial Edge NXT® allows organizations to separate and track the key components of an endowment: the original corpus, the accumulated earnings, and the spendable balance. Because these amounts are maintained within a single system, the finance office can quickly see what is available to spend and how to align with the donor restrictions.

With system-generated reports, organizations can produce consistent, accurate views of fund activity for board members, auditors, development officers, and donors without rebuilding templates or reconciling spreadsheets. This level of transparency strengthens internal communication and supports better stewardship conversations.

Integrated systems also improve the workflow between finance and development. When both teams are looking at the same data, spending decisions become more straightforward, and the organization can respond quickly to questions about fund availability and donor intent.

With the right technology in place, organizations eliminate guesswork and reduce manual effort, allowing more time to focus on putting the endowed resources to work. Fund accounting software not only makes endowment management easier, but it also ensures that each dollar is used appropriately and effectively to advance the mission.

Best Practices for Managing Spendable Balances in Your Endowment

Managing spendable balances effectively requires systems and processes that give finance teams clarity, consistency, and reliable information. The goal is simple: make it easy to know what can be spent and how it aligns with donor intent. The following best practices help to ensure strong endowment stewardship:

Segment fund activity clearly and consistently

Use a fund accounting system that allows you to maintain the original gift amount, accumulated earnings, and the spendable balance as distinct components. When these elements are tracked separately, it becomes easier to confirm availability, explain calculations, and support decisions.

Leverage multi-dimensional coding

Tools such as project codes, transaction codes, fund segments, transaction attributes, or class segments make it possible to analyze endowment activity across multiple views to meet the needs of various stakeholders, including donors, board members, auditors, and beneficiaries.

Review spendable balances regularly

Spendable balances should not sit unnoticed until year-end. Establish a regular schedule to review your endowed funds. Confirm spendable amounts and identify deficiencies or balances that are sitting unused. Routine reviews ensure problems are caught early, and opportunities aren’t missed.

Tailor reporting to the correct audience

Donors benefit from clear, concise updates that highlight mission impact. Leadership needs summaries that inform planning and strategic allocation of resources. Auditors require detailed transaction-level data and visibility into how spending aligns with policies and donor intent. Departments need to know what is available to spend on scholarships, programs, and research.

Integrate your fundraising CRM with your accounting system

When gifts flow automatically into the financial system, you reduce the risk of errors drastically. This ensures the finance office always has the most up-to-date information without a lot of manual work or reconciliations.

Document your process and keep it consistent

Clear procedures for calculating, reviewing, and communicating spendable balances reduce inconsistency and ensure that everyone is following the same playbook. This is especially important during leadership transitions or staffing changes.

By adopting these best practices, organizations reduce errors, increase transparency, and build a stronger culture of stewardship. Most importantly, they ensure that endowed resources are used fully and appropriately to support the mission.

Elevating Trust and Stewardship Through Effective Spendable Balance Management

Effective management of spendable balances is a core stewardship practice that shapes how well an organization fulfills its mission. When finance teams have visibility into the data, they create a reliable framework for decision-making. When those numbers are communicated consistently and verified through strong systems, programs receive the resources they need, donors gain confidence, and leadership has a clear view of the organization’s long-term capacity.

Purpose-built fund accounting tools make this work possible. By replacing manual processes with structured, transparent data, finance offices eliminate guesswork, reduce risk, and ensure that every spending decision aligns with donor intent, organizational policy, and regulatory requirements. Integrated systems and well-designed reporting strengthen collaboration across departments and allow the organization to demonstrate responsible stewardship at every level.

When spendable balances are managed thoughtfully and consistently, the impact is tangible. More dollars actively supporting the mission, fewer compliance concerns, and a stronger foundation of trust with donors, auditors, and internal stakeholders. Accountability and transparency matter more than ever, so mastering spendable balance management positions your organization to use its endowment resources wisely and to deliver lasting value to the communities you serve.

Learn more about how fund accounting solutions like Financial Edge NXT can transform your endowment accounting for improved impact.