How to Improve Your Internal Controls to Minimize Audit Findings

Navigating the process of preparing for an audit can be a daunting task. The time and resources needed can be significant, especially with respect to internal controls. Not having sufficient control documentation can create a more time-consuming process and lead to your external auditors identifying recommendations or deficiencies.

Internal controls are an area of heavy focus during financial statement audits. Having a strong set of internal controls can make the audit process smoother for your organization, with fewer audit findings.

Why Your Organization Needs Effective Internal Controls

An effective system of internal controls is essential for any nonprofit organization, whether you are required to have an annual financial audit or not. By implementing and maintaining strong internal controls, you can protect your organization from financial loss and reputational damage.

Here are a few reasons why internal controls are especially important for nonprofit organizations:

- Safeguarding Assets: Nonprofits often have limited resources and rely heavily on donations and grants. Internal controls help protect these assets from fraud, theft, and misuse, ensuring that funds are used for their intended purposes.

- Financial Accountability: Donors, grantors, and the public trust nonprofits to manage their finances responsibly. Strong internal controls promote financial transparency and accountability, demonstrating that funds are being used ethically and effectively.

- Compliance with Laws and Regulations: Nonprofits must comply with various laws and regulations, including those related to tax-exempt status, fundraising, and financial reporting. Internal controls help ensure compliance, avoiding penalties and maintaining the organization’s reputation.

- Operational Efficiency: Effective internal controls streamline operations, reduce errors, and improve efficiency, allowing nonprofits to focus on their core mission and programs.

- Risk Management: Internal controls help identify and mitigate risks, protecting the organization from financial loss and reputational damage.

A strong system of internal controls helps your organization run smoothly and creates clear expectations for your staff and leadership.

Internal Controls and Financial Audits

Strong and effective internal controls will make for a smoother audit from start to finish. Internal controls are crucial for financial audits. They make sure your organization proactively adheres to accounting best practices and are a key focus for auditors to verify their effectiveness. Robust internal controls streamline the entire audit process.

Here are a few elements of internal controls to keep in mind when you are preparing for your audit.

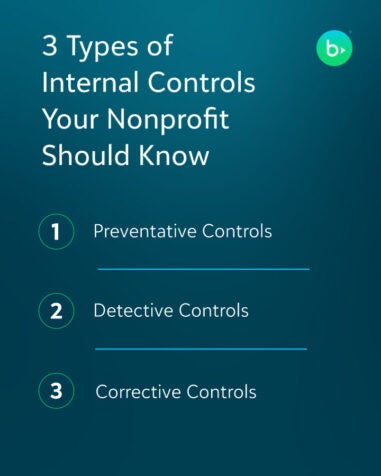

Types of Internal Controls

Internal controls can be categorized into several types. The different types work together to make sure you have processes in place to prevent, identify, and fix potential issues. Your auditor will be looking for all three types.

- Preventive controls are designed to deter errors or irregularities from occurring in the first place. Examples include segregation of duties, authorization requirements, and physical safeguards.

- Detective controls are designed to identify errors or irregularities that have already occurred. Examples include reconciliations, audits, and exception reports.

- Corrective controls are designed to remedy errors or irregularities that have been detected. Examples include backup procedures, disciplinary action, and insurance.

Some of these types can be managed directly within your fund accounting software, such as approval rules to make sure the right people review an expense before it’s paid. But some of these controls, such as what happens if a check is stolen, will need to be part of your process documentation.

Components of Effective Internal Controls

For each of your internal controls, your auditor will be looking to see if they are set up correctly and effectively. Below are the key components of internal controls:

- Your control environment sets the tone for the organization’s commitment to internal controls, including ethical values, management philosophy, and organizational structure.

- A regular risk assessment involves identifying and evaluating internal and external risks that could affect the organization’s ability to achieve its objectives.

- Your control activities are the specific policies and procedures you implement to mitigate risks and achieve organizational objectives, such as spending limits on your purchase cards.

- You need information and communication systems and processes in place for collecting, processing, and communicating information relevant to internal controls.

- Monitoring systems provide ongoing evaluation of the effectiveness of internal controls and making necessary adjustments.

Implementing Internal Controls

If you are putting internal controls in place for the first time, or you want to establish new controls, here are a few important steps to implementing internal controls.

- Assess Risks: Identify the risks that could impact the organization’s operations and finances.

- Develop Policies and Procedures: Create written policies and procedures that address identified risks and outline control activities.

- Train Staff: Provide training to staff on internal control policies and procedures.

- Monitor and Evaluating: Regularly monitor and evaluate the effectiveness of internal controls and make necessary adjustments.

By implementing strong internal controls, nonprofit organizations can ensure the responsible and effective use of resources, maintain financial integrity, and achieve their missions, ultimately making a greater impact in their communities.

Internal Control Checklist for Your Financial Audit

With good preparation, your annual financial audit can be straightforward and stress-free. Below is a checklist of key areas that you should review when establishing or evaluating your internal control system before an audit.

These are areas that external auditors will focus on when conducting their audit procedures. Taking the time to ensure that these areas have appropriate controls will go a long way towards making the audit process smoother for all who are involved.

- Segregation of Duties: No one person should have control over all aspects of a financial transaction. Different individuals should be responsible for authorizing, recording, and reconciling transactions to prevent fraud and errors.

- Cash Management: Cash is the most liquid asset and therefore most susceptible to theft. Implement strict controls over cash handling, including proper authorization for disbursements, regular bank reconciliations, and surprise cash counts.

- Grant and Donation Management: Ensure that grants and donations are properly recorded, tracked, and used for their intended purposes. Maintain documentation of donor restrictions and ensure compliance with grant requirements.

- Payroll: Implement controls to verify accurate payroll processing, including proper authorization of time sheets, verification of employee information, and timely tax filings.

- Expense Reimbursements: Establish clear policies and procedures for expense reimbursements, including documentation requirements, approval processes, and limits on reimbursable expenses.

- Fixed Assets: Maintain a detailed inventory of fixed assets, including descriptions, locations, and values. Conduct periodic physical inventories to verify the existence and condition of assets.

- Financial Reporting: Prepare accurate and timely financial reports that comply with accounting standards and regulatory requirements. Ensure that your management or board review and approve financial statements regularly.

- Risk Assessment: Regularly assess the organization’s risks and identify potential areas of weakness in the internal control system. Update controls as needed to address emerging risks.

- Whistleblower Policy: Establish a confidential reporting mechanism for employees and volunteers to report suspected fraud or unethical behavior without fear of retaliation.

- Training and Education: Provide ongoing training and education to staff and volunteers on internal control policies and procedures, as well as the importance of ethical behavior.

- Board Oversight: The board of directors should provide oversight of the organization’s internal control system and ensure that it is functioning effectively. This can include, but is not limited to, an annual review of internal controls by this governing body.

- External Audits: Periodic external financial audits by an independent accounting firm can provide assurance on the effectiveness of the organization’s internal controls and identify areas for improvement.

Strong Internal Controls Simplify Your Annual Financial Audit

Remember that strong internal controls are not a one-time project but an ongoing process. By implementing and maintaining effective internal controls, nonprofit organizations can protect their assets, ensure compliance, and build a strong foundation for achieving their mission. And as an added bonus, they can make your financial statement audit a more efficient and effective process for all involved.

Looking for a fund accounting system that helps you implement and enforce strong internal controls? Check out our guide, 3 Ways Your Fund Accounting System Helps Create Strong Internal Controls.

Free Guide

8 Ways Fund Accounting Software Helps You Improve Compliance and Revenue Tracking